The long game: The Dollar, Gold and US Treasuries

In the short term, the Fed and US Treasury manipulate the Dollar and US Treasury yields in an attempt to stimulate the economy while avoiding inflation. Foreign central banks also attempt to manipulate the Dollar to gain a trade advantage, which impacts the Treasury market. However, in the long term, large secular trends lasting several decades will likely determine the direction of US financial markets and fuel a bull market for gold.

Short-term Outlook

Inflation has moderated, with CPI falling below 3.0%, allowing the Fed to cut interest rates. The fall in headline CPI (red, right-hand scale) was precipitated by a sharp decline in energy prices (orange, left-hand scale).

However, inflation could rebound if geopolitical tensions restrict supply or demand grows due to an economic recovery in China and Europe or further expansion in the US.

The Fed has cut its interest rate target by 1.0% from its 2024 peak to stimulate economic activity.

Efforts to normalize monetary policy have reduced Fed holdings of Treasury and mortgage-backed securities by $2 trillion. This would typically contract liquidity, stressing financial markets.

However, the Fed neutralized its QT operations by reducing overnight reverse repo (RRP) liabilities by nearly $2.3 trillion. Money market funds were encouraged to invest in the enormous flood of T-bills issued by Janet Yellen at the US Treasury instead of in reverse repo from the Fed. The simultaneous reduction in UST assets and RRP liabilities on the Fed's balance sheet left financial market liquidity unscathed.

Long-term Treasury yields climbed despite the Fed reducing short-term rates, indicating bond market fears of an inflation rebound. However, a benign December reading for services CPI (below) triggered a retracement.

Respect of support at 4.5% will likely signal an advance to test resistance at 5.0% on the 10-year Treasury yield below.

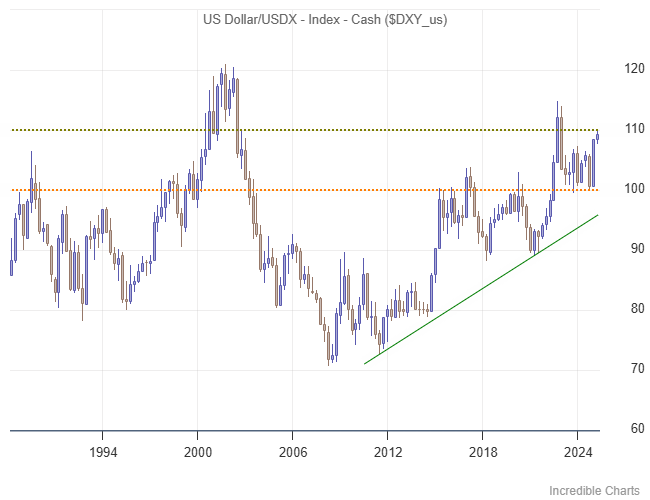

The Dollar Index found support at 109 and is expected to re-test resistance at 110. The strong Dollar increases pressure on foreign central banks to sell off reserves to defend their currencies, driving up yields as foreign selling of Treasuries grows.

Gold is trending upwards despite rising Treasury yields and the strong Dollar. Breakout above $2,800 per ounce would offer a medium-term target of $3,000.

The Long Game

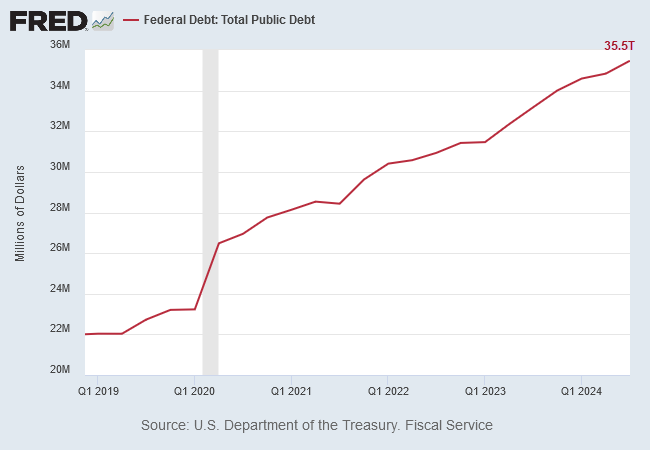

The elephant in the room is US federal debt, which had grown to $35.5 trillion at the end of Q3 in 2024.

Fiscal deficits are widening, with interest servicing costs recently overtaking defense spending in the budget.

Federal debt (red below) is growing faster than GDP (blue), warning that the fiscal position is unsustainable, especially as interest servicing costs widen the gap.

The ratio of federal debt to GDP grew to a precarious 113.3 percent at the end of Q3 2024 and is expected to accelerate higher.

Long-term Treasury yields are rising as concerns grow over the unsustainability of debt and deep fiscal deficits fueling long-term inflation.

The strong Dollar further exacerbates the situation, increasing sales of US Treasuries, as mentioned earlier, when foreign central banks free up reserves to protect their currencies. The incoming Republican administration has committed to preserving the Dollar's status as the global reserve currency. Maintaining reserve currency status is likely to entrench a strong Dollar. A Dollar index breakout above 110 will offer a target of the high at 120 from 2000, as shown on the quarterly chart below.

As Luke Gromen points out, the Fed can cut interest rates to weaken the Dollar, but that would increase fears of inflation and, in turn, drive up Treasury yields. So, the rise in long-term Treasury yields is almost inevitable.

Gold respected support at $2,600 per ounce, as shown on the monthly chart below. The secular uptrend is fueled by four key concerns. First is the sustainability of US federal debt. Next is fear of rising inflation exacerbated by the on-shoring of critical supply chains and a decline in international trade. Third are geopolitical tensions, fostering rising demand for the safety of gold and an increased desire by non-aligned nations to break free from Dollar hegemony. Last is the collapsing Chinese real estate market, which no longer serves as the primary investment for private savings, leaving gold the most attractive alternative.

Breakout above $2,800 would offer a long-term target of $3,600 per ounce.

Conclusion

Treasury yields are in a secular uptrend, with the bond bear market expected to last at least a decade. The primary driver is concern over the sustainability of US federal debt, which exceeds 110% of GDP, while deficits threaten to expand. Not far behind are fears of rising long-term inflation, fueled by expanding fiscal deficits while the economy is close to full employment, and increased protectionism driving up costs.

The Dollar is likely to remain strong, with the Index expected to reach 120, as long as the US remains committed to preserving the Dollar's status as the global reserve currency.

Gold is riding a secular wave, fueled by concerns over the sustainability of US federal debt, fears of long-term inflation, rising geopolitical tensions, and collapse of the domestic real estate market as an attractive investment for private Chinese savings. We expect this to last for decades, perhaps even longer. Our target for gold is $3,600 per ounce by 2028.

The only feasible long-term path to reduce federal debt relative to GDP is for the Fed to suppress interest rates. This would allow GDP fueled by inflation to grow at a faster rate than fiscal debt and gradually reduce the ratio of debt to GDP to sustainable levels. The inevitable negative real interest rates would further boost demand for gold.

Acknowledgments

- CBO: The Budget and Economic Outlook: 2025 to 2035

- Bureau of the Fiscal Service: Monthly Treasury Statement

- Luke Gromen, FFTT: January 17, 2025

Market Analysis Subscribers

Everything contained in this email, related websites, training videos and training courses (collectively referred to as the "Material") has been written for the purpose of teaching analysis, trading and investment techniques. The Material neither purports to be, nor is it intended to be, advice to trade or to invest in any financial instrument, or class of financial instruments, or to use any particular methods of trading or investing.

Advice in the Material is provided for the general information of readers and viewers (collectively referred to as "Readers") and does not have regard to any particular person's investment objectives, financial situation or needs. Accordingly, no Reader should act on the basis of any information in the Material without properly considering its applicability to their financial circumstances. If not properly qualified to do this for themselves, Readers should seek professional advice.

Investing and trading involves risk of loss. Past results are not necessarily indicative of future results.

You, the Reader, need to conduct your own research and decide whether to invest or trade. The decision is yours alone. We expressly disavow all and any liability to any person, with respect of anything, and of the consequences of anything, done or omitted to be done by any such person in reliance upon the whole or any part of the Material.

Author: Colin Twiggs is a former investment banker with almost 40 years of experience in financial markets. He co-founded Incredible Charts and writes the popular Trading Diary and Patient Investor newsletters.

Using a top-down approach, Colin identifies key macro trends in the global economy before evaluating selected opportunities using a combination of fundamental and technical analysis.

Focusing on interest rates and financial market liquidity as primary drivers of the economic cycle, he warned of the 2008/2009 and 2020 bear markets well ahead of actual events.

He founded PVT Capital (AFSL No. 546090) in May 2023, which offers investment strategy and advice to wholesale clients.