A stock market bubble of epic proportions

First, please read the Disclaimer.

A great deal has been written in recent years about real estate bubbles, stock market bubbles and even bond market bubbles. But there is really only one kind of bubble — that is a debt bubble. Without low interest rates fueling rapid debt growth, any form of bubble would wither on the vine.

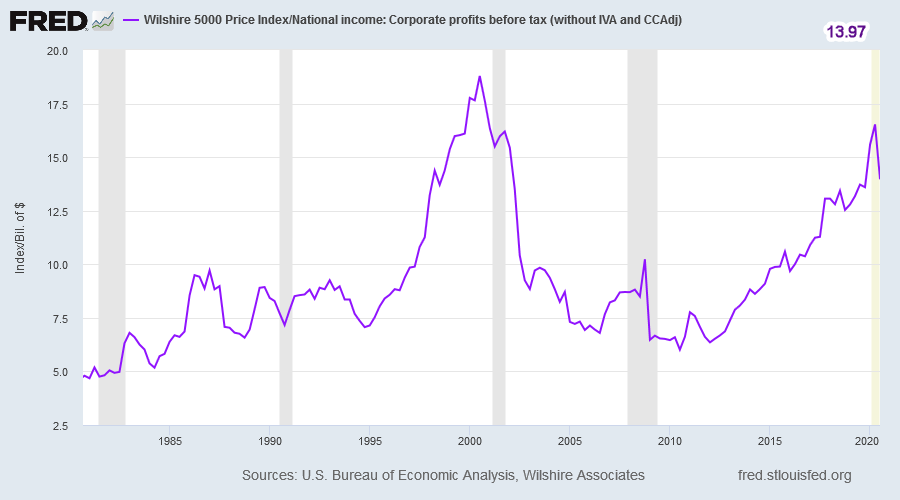

The Wilshire 5000 broad market index, compared to profits before tax, recently peaked above 15.0 for only the second time in history before retreating to 13.97 in Q3. The fall in Q3 is attributable to recovering profits rather than falling stock prices, so a return to above 15.0 seems likely if the index rises in response.

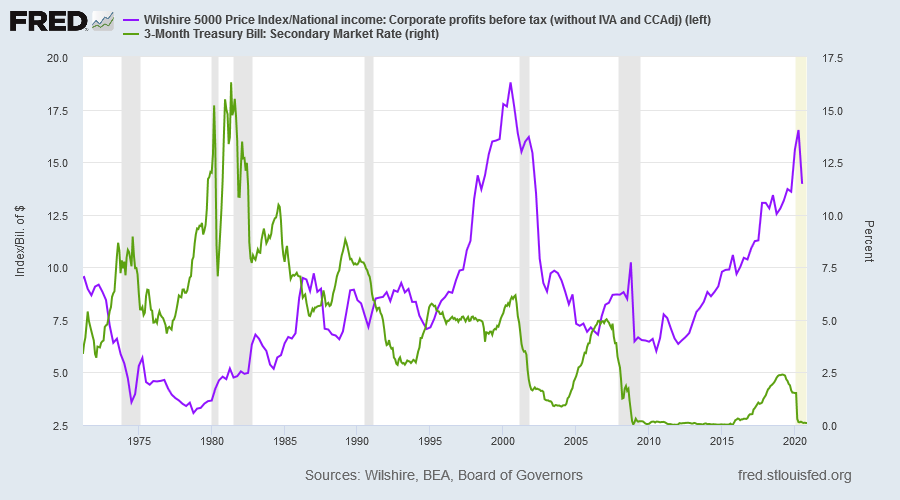

The reason for the surge in stock prices is clear on the chart below: interest rates at close to zero for an extended period act like rocket fuel.

Anna Schwartz, co-author of A Monetary History of the United States (with Milton Friedman, 1963) once said:

If you investigate individually the manias that the market has so dubbed over the years, in every case, it was expansive monetary policy that generated the boom in an asset. The particular asset varied from one boom to another. But the basic underlying propagator was too-easy monetary policy and too-low interest rates.

That is particularly true of the current bubble.

When will it end?

The Fed seems unlikely to change course and is expected to keep interest rates near zero for an extended period, so when is the bubble likely to end?

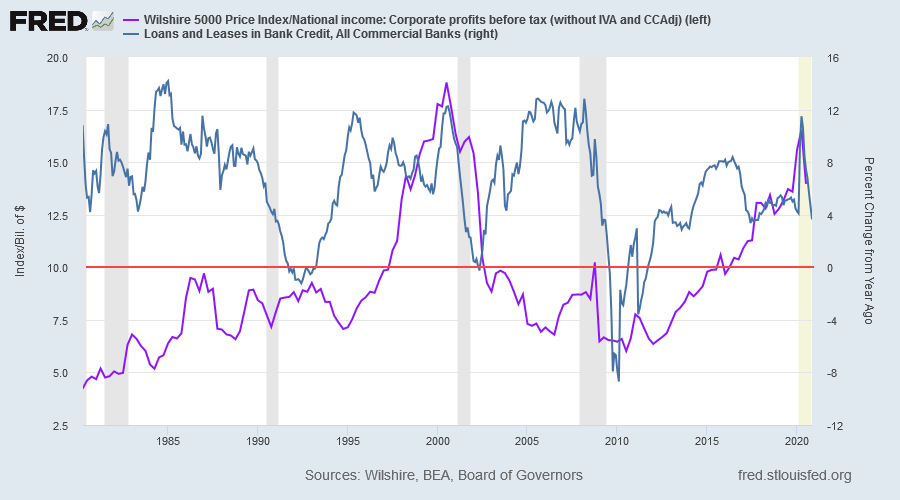

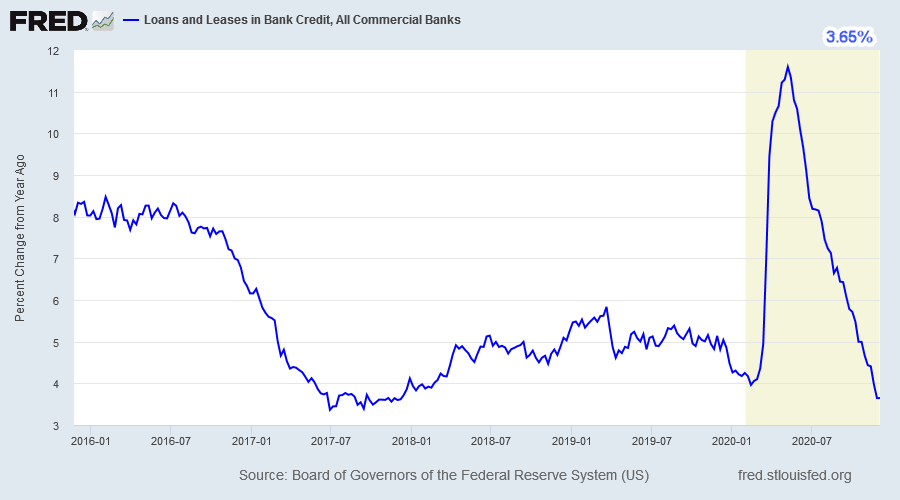

If bank credit growth stalls, falling to zero (the red line) as it did before the last three recessions, stock prices are likely to tumble.

There may be three possible causes of slowing credit growth:

- Inflation surges, forcing the Fed to raise interest rates;

- Low interest rates cause investment misallocation, as in the Dotcom and subprime bubbles, leading to rising defaults and tighter bank credit; or

- An external shock causes falling aggregate demand and high unemployment, with banks tightening credit policies in anticipation of rising defaults.

Chairman Jay Powell has assured us that the Fed will tolerate higher inflation, with its new policy of inflation averaging, so higher interest rates do not seem to be a major risk. While there has been some investment misallocation, falling aggregate demand and high unemployment seem to be the greatest threat.

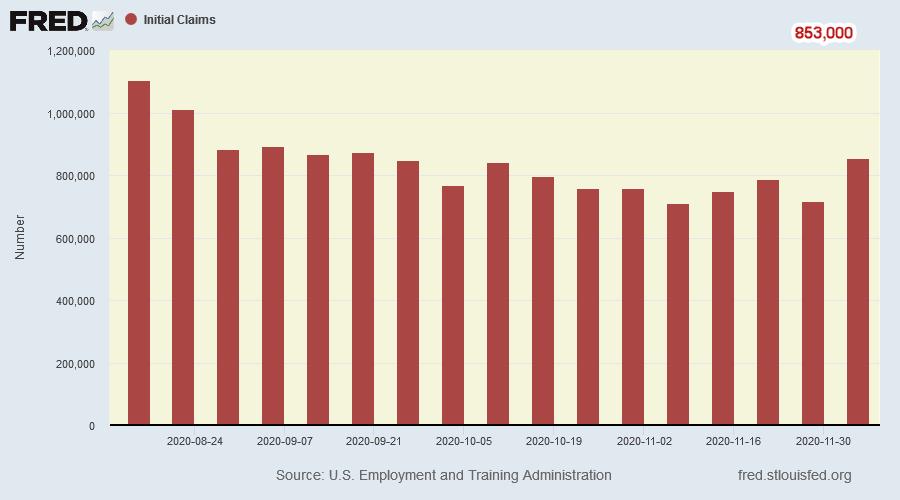

Initial claims for unemployment insurance jumped to 853,000 for the week ended December 5th, while initial claims for pandemic unemployment assistance surged to 427,600.

Latest Department of Labor figures (November 21) show total unemployment claims remain high at 19 million — or 1 in 8 people who had a job in February 2020.

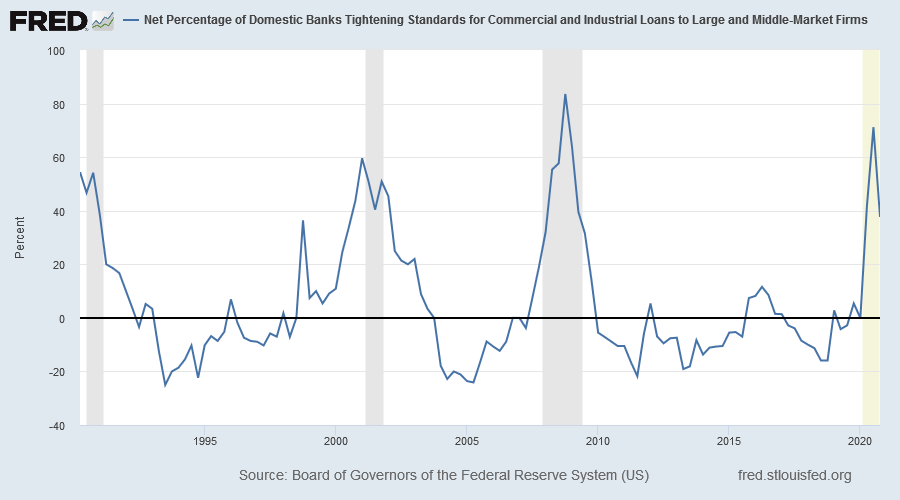

Bank credit standards have tightened significantly.

Conclusion

Keep a close watch on bank credit growth. If this falls to zero, then stock prices are likely to tumble.

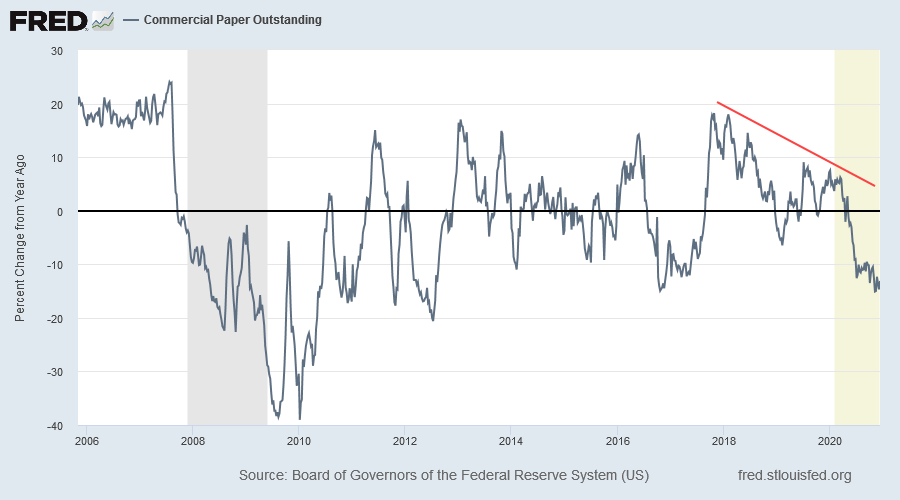

Commercial paper often acts as the canary in the coal mine, giving advance warning of a credit contraction.

Quote for the Week

"The more spectacular the rise and the longer it goes, the more certainty one can have that you're in the 'Real McCoy' bubble. You want to see lots of crazy behavior, which we really have seen a lot of ....and you want to see not just the market rise, but if anything, an acceleration. And the rate of market rise, since the turn in March/April, has been nothing sort of sensational."

~ Jeremy Grantham, co-founder and chief investment strategist of GMO, November 12, 2020

Updates for Market Analysis Subscribers

Please take advantage of our $1 special offer for the first month. Cancel at any time.

Disclaimer

Colin Twiggs is director of The Patient Investor Pty Ltd, an Authorised Representative (no. 1256439) of MoneySherpa Pty Limited which holds Australian Financial Services Licence No. 451289.

Everything contained in this web site, related newsletters, training videos and training courses (collectively referred to as the "Material") has been written for the purpose of teaching analysis, trading and investment techniques. The Material neither purports to be, nor is it intended to be, advice to trade or to invest in any financial instrument, or class of financial instruments, or to use any particular methods of trading or investing.

Advice in the Material is provided for the general information of readers and viewers (collectively referred to as "Readers") and does not have regard to any particular person's investment objectives, financial situation or needs. Accordingly, no Reader should act on the basis of any information in the Material without properly considering its applicability to their financial circumstances. If not properly qualified to do this for themselves, Readers should seek professional advice.

Investing and trading involves risk of loss. Past results are not necessarily indicative of future results.

The decision to invest or trade is for the Reader alone. We expressly disclaim all and any liability to any person, with respect of anything, and of the consequences of anything, done or omitted to be done by any such person in reliance upon the whole or any part of the Material.

Please read the Financial Services Guide.

Author: Colin Twiggs is a former investment banker with almost 40 years of experience in financial markets. He co-founded Incredible Charts and writes the popular Trading Diary and Patient Investor newsletters.

Using a top-down approach, Colin identifies key macro trends in the global economy before evaluating selected opportunities using a combination of fundamental and technical analysis.

Focusing on interest rates and financial market liquidity as primary drivers of the economic cycle, he warned of the 2008/2009 and 2020 bear markets well ahead of actual events.

He founded PVT Capital (AFSL No. 546090) in May 2023, which offers investment strategy and advice to wholesale clients.