S&P 500 and the trade war

By Colin Twiggs

May 24, 2019 11:30 p.m. EDT (1:30 p.m. AEST)

First, please read the Disclaimer.

We are now headed for a full-blown trade war. Donald Trump may have highlighted the issue but this is not a conflict between him and Xi -- it should have been addressed years ago -- nor even between China and the West. Accusations of racism are misguided. This is a conflict between totalitarianism and the rule of law. Between the CCP (with Putin, Erdogan, and the Ayatollahs in their corner) and Western democracy.

Australia will be forced to take sides. China may be Australia's largest trading partner but the US & UK are it's ideological partners. I cannot see the remotest possibility of Australia selling out its principles for profits, no matter how tempting the short-term rewards (or threatened hardships). We have a proud history of standing up against oppression and exploitation.

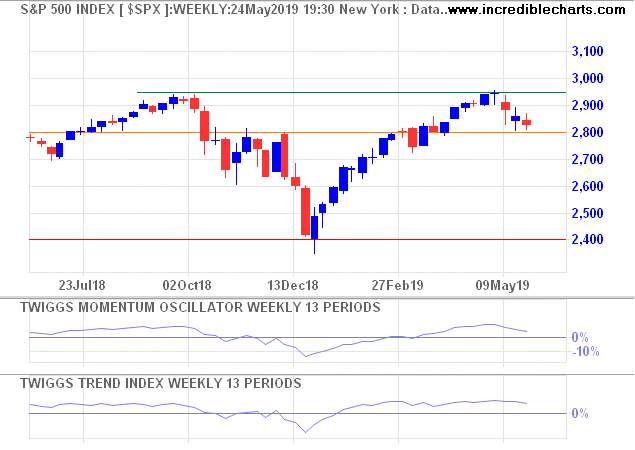

Disruptions to supply chains and supply contracts in the US (and China) are going to be significant and are likely to impact on earnings. The S&P 500 reaction is so far muted, with retracement testing medium-term support at 2800. There is also no indication of selling pressure on the Trend Index. Nevertheless, a breach of 2800 is likely and would warn of a test of primary support at 2400.

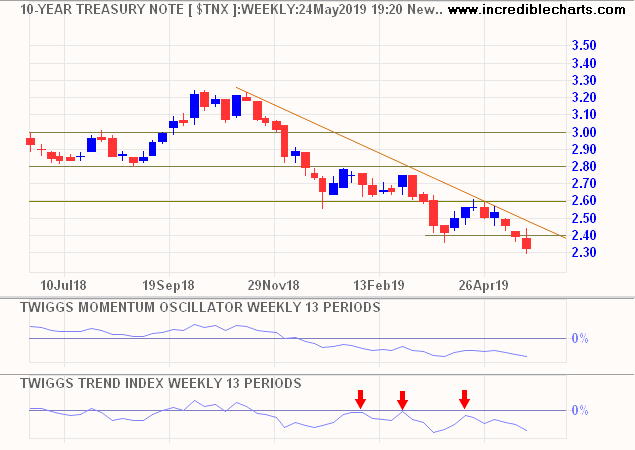

Falling Treasury yields highlight the outflow from equities and into bonds. Stock buybacks are becoming the primary inflow into stocks.

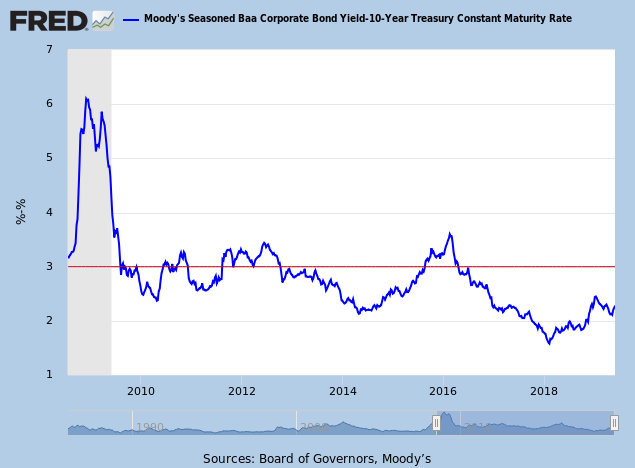

However, corporate bond spreads -- lowest investment grade (Baa) yields minus the equivalent Treasury yield -- are still well below the 3.0% level associated with elevated risk.

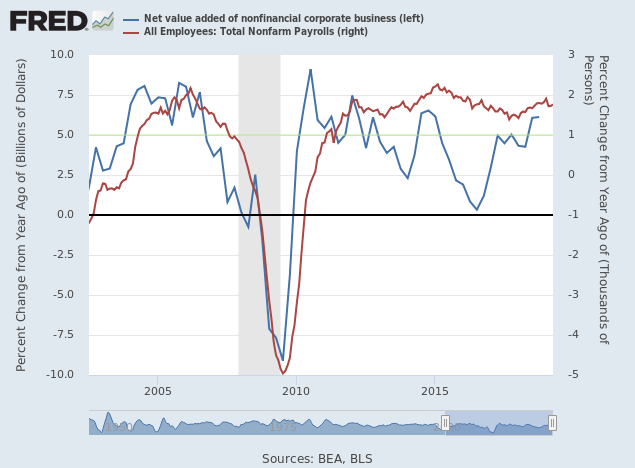

Profits may fall due to supply disruption (similar to 2015 on the chart below) but the Fed is unlikely to cut interest rates unless employment follows (as in 2007). Inflation is likely to rise as supply chains are disrupted but chances of a rate rise are negligible. Fed Chairman Jay Powell's eyes are going to be firmly fixed on Total Non-farm Payrolls. If annual growth falls below 1.0% (RHS), expect a rate cut.

This excerpt from a newsletter I wrote in April 2018 (Playing hardball with China) is illuminating: "In 2010, Paul Krugman wrote:

Krugman now seems more opposed to trade tariffs but observes:Some still argue that we must reason gently with China, not confront it. But we've been reasoning with China for years, as its surplus ballooned, and gotten nowhere: on Sunday Wen Jiabao, the Chinese prime minister, declared -- absurdly -- that his nation's currency is not undervalued. (The Peterson Institute for International Economics estimates that the renminbi is undervalued by between 20 and 40 percent.) And Mr. Wen accused other nations of doing what China actually does, seeking to weaken their currencies 'just for the purposes of increasing their own exports.'

But if sweet reason won't work, what's the alternative? In 1971 the United States dealt with a similar but much less severe problem of foreign undervaluation by imposing a temporary 10 percent surcharge on imports, which was removed a few months later after Germany, Japan and other nations raised the dollar value of their currencies. At this point, it's hard to see China changing its policies unless faced with the threat of similar action -- except that this time the surcharge would have to be much larger, say 25 percent.

I don't propose this turn to policy hardball lightly. But Chinese currency policy is adding materially to the world's economic problems at a time when those problems are already very severe. It's time to take a stand.

....I think it's worth noting that even if we are headed for a full-scale trade war, conventional estimates of the costs of such a war don't come anywhere near to 10 percent of GDP, or even 6 percent. In fact, it's one of the dirty little secrets of international economics that standard estimates of the cost of protectionism, while not trivial, aren't usually earthshaking either."Trump has to show that he is prepared to endure the hardships of a trade war and not kowtow to Beijing. But Beijing is unlikely to back down either.

Men naturally despise those who court them, but respect those who do not give way to them.

~ Thucydides (circa 400 BC)

Latest

-

ASX 200

ASX 200 rises despite the falling Dollar. -

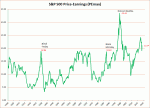

S&P 500 Price-Earnings Ratio

S&P 500 Price-Earnings Ratio

Is the S&P 500 way over-priced? -

Gold

Gold

Gold at a watershed. -

PEmax

Why you should be wary of Robert Shiller's CAPE -

Portfolio

Investing in a volatile market - April 2018

Disclaimer

Colin Twiggs is director of The Patient Investor Pty Ltd, an Authorised Representative (no. 1256439) of MoneySherpa Pty Limited which holds Australian Financial Services Licence No. 451289.

Everything contained in this web site, related newsletters, training videos and training courses (collectively referred to as the "Material") has been written for the purpose of teaching analysis, trading and investment techniques. The Material neither purports to be, nor is it intended to be, advice to trade or to invest in any financial instrument, or class of financial instruments, or to use any particular methods of trading or investing.

Advice in the Material is provided for the general information of readers and viewers (collectively referred to as "Readers") and does not have regard to any particular person's investment objectives, financial situation or needs. Accordingly, no Reader should act on the basis of any information in the Material without properly considering its applicability to their financial circumstances. If not properly qualified to do this for themselves, Readers should seek professional advice.

Investing and trading involves risk of loss. Past results are not necessarily indicative of future results.

The decision to invest or trade is for the Reader alone. We expressly disclaim all and any liability to any person, with respect of anything, and of the consequences of anything, done or omitted to be done by any such person in reliance upon the whole or any part of the Material.

Please read the Financial Services Guide.

Author: Colin Twiggs is a former investment banker with almost 40 years of experience in financial markets. He co-founded Incredible Charts and writes the popular Trading Diary and Patient Investor newsletters.

Using a top-down approach, Colin identifies key macro trends in the global economy before evaluating selected opportunities using a combination of fundamental and technical analysis.

Focusing on interest rates and financial market liquidity as primary drivers of the economic cycle, he warned of the 2008/2009 and 2020 bear markets well ahead of actual events.

He founded PVT Capital (AFSL No. 546090) in May 2023, which offers investment strategy and advice to wholesale clients.