Fed rate hike or no hike?

By Colin Twiggs

June 1st, 2017 9:00 p.m. EDT (11:00 a.m. AEST)

First, please read the Disclaimer.

From Marc Chandler in Marc to Market:

In between the North Korean summit and the details of the US tariffs on Chinese goods, both the Federal Reserve and the ECB meet. There should be little doubt that the Federal Reserve will hike rates by 25 bp [in June], raising the new target range to 1.75%-2.00%. The Fed has signaled that it will no longer pay interest on reserves at the upper end of the Fed funds range, but five bp below.

For

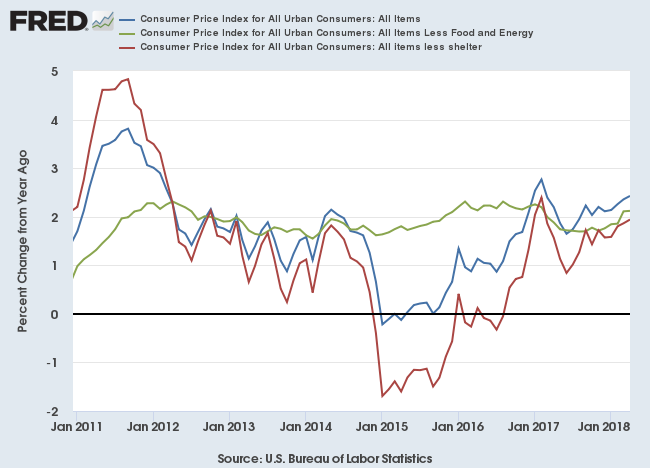

The Consumer Price Index, including Core CPI (ex Food and Energy) and CPI ex Shelter, started creeping upwards in April. A higher May figure would strengthen Fed resolve.

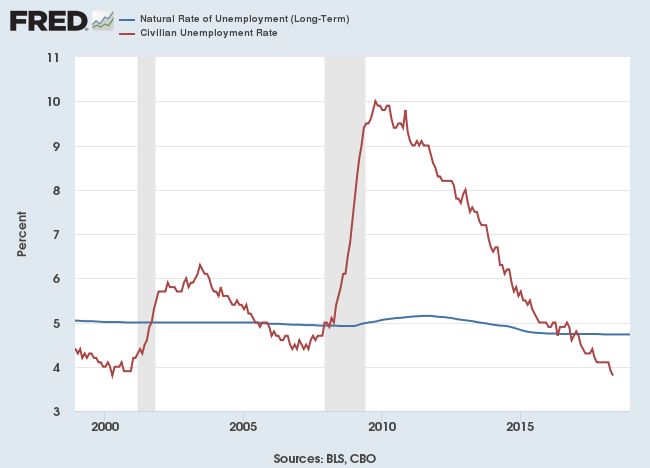

May employment figures show Unemployment falling to its April 2000 low of 3.8 percent. Unemployment below the long-term natural rate of unemployment is expected to increase upward pressure on wages.

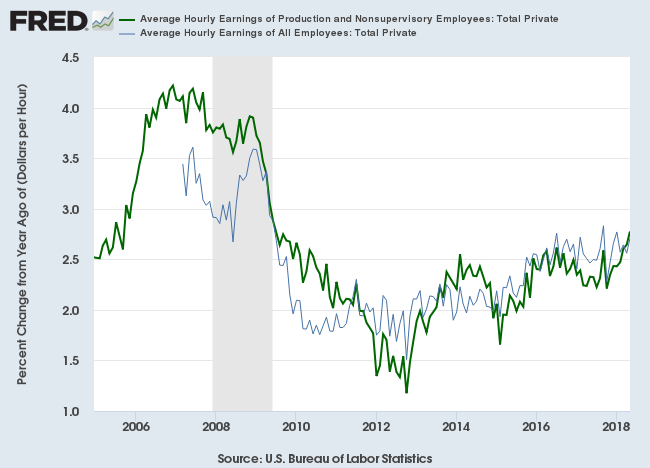

Average hourly wage rates for May have turned upwards, with the average rate for production and non-supervisory employees in the private sector reaching an annual growth rate of 2.78 percent. The Fed still has some discretion but growth above 3.0 percent would force their hand.

Against

Earlier in the week the case for no rate hike was a lot stronger, with political turmoil in Italy and a no-confidence vote in Spain threatening stability of the European Monetary Union. But a few days can make a big difference as Marc reports:

The week is ending quite a bit different than it began. The main banking concern is not in Italy but in German, where shares in Deutsche Bank shares fell to a record low yesterday, and S&P Global cut its credit rating one step to BBB+ (third-lowest investment grade).

The political angst is not focused on Rome but Madrid, where Rajoy lost a vote of confidence A Socialist-led government is also seen likely to call for elections before the end of the year. None of the major parties in Spain are antagonistic to the EU or the EMU. This year's budget was passed in late May, so there is no sense of urgency in an economy that remains one of the stronger performers in the union.

Despite the first populist-led government in Europe taking office today, Italian debt markets continue to recover from the multi-sigma shock seen earlier in the week. Italy's two-year yield is off 30 bp today, leaving it up about 22 bp on the week. The 10-year yield is off 19 bp to 2.56%. This represents a 10 bp decline on the week. Spain's 10-year benchmark yield is off eight basis points this week. Similarly, Italian stocks are outperforming, and among the best performing bourses. Italy's Milan is up 2.7% to nearly recoup the loss on the week....

Expect Fed rate hikes to continue at a steady pace unless there is a sharp spike in underlying inflation, reflected by average wage rate growth rising above 3.0 percent. In that case, rate hikes would be expected to quicken.

There is one side to the stock market; and it is not the bull side or bear side, but the right side.

~ Jesse Livermore

Latest

-

S&P 500 and Nasdaq 100

Nasdaq bull signal. -

ASX 200

Bi-polar ASX continues. -

Gold

Dollar resistance and weaker bond yields a reprieve. -

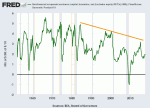

The Yield Curve

Low inflation risk keeps yield curve safe. -

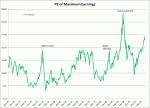

Price & Earnings

The Race to the Top -

US & Global economy

Is GDP doomed to low growth? -

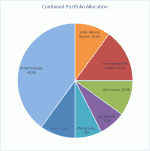

Investing in a Volatile Market

Managing downside risk.

Disclaimer

Colin Twiggs is director of The Patient Investor Pty Ltd, an Authorised Representative (no. 1256439) of MoneySherpa Pty Limited which holds Australian Financial Services Licence No. 451289.

Everything contained in this web site, related newsletters, training videos and training courses (collectively referred to as the "Material") has been written for the purpose of teaching analysis, trading and investment techniques. The Material neither purports to be, nor is it intended to be, advice to trade or to invest in any financial instrument, or class of financial instruments, or to use any particular methods of trading or investing.

Advice in the Material is provided for the general information of readers and viewers (collectively referred to as "Readers") and does not have regard to any particular person's investment objectives, financial situation or needs. Accordingly, no Reader should act on the basis of any information in the Material without properly considering its applicability to their financial circumstances. If not properly qualified to do this for themselves, Readers should seek professional advice.

Investing and trading involves risk of loss. Past results are not necessarily indicative of future results.

The decision to invest or trade is for the Reader alone. We expressly disclaim all and any liability to any person, with respect of anything, and of the consequences of anything, done or omitted to be done by any such person in reliance upon the whole or any part of the Material.

Author: Colin Twiggs is a former investment banker with almost 40 years of experience in financial markets. He co-founded Incredible Charts and writes the popular Trading Diary and Patient Investor newsletters.

Using a top-down approach, Colin identifies key macro trends in the global economy before evaluating selected opportunities using a combination of fundamental and technical analysis.

Focusing on interest rates and financial market liquidity as primary drivers of the economic cycle, he warned of the 2008/2009 and 2020 bear markets well ahead of actual events.

He founded PVT Capital (AFSL No. 546090) in May 2023, which offers investment strategy and advice to wholesale clients.