Why is the Dollar falling?

By Colin Twiggs

February 23, 2017 1:00 a.m. EST (6:00 p.m. AEDT)

Please read the Disclaimer.

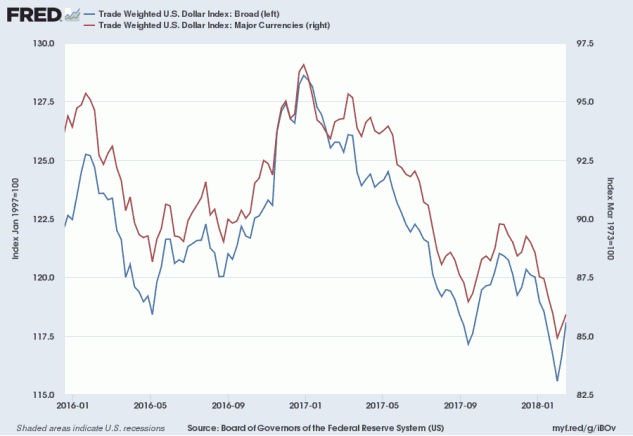

The broad, trade-weighted US Dollar index has been declining since early 2017.

This is the best explanation I have found for current US Dollar weakness. From Bank of Montreal, BMO Nesbitt Burns:

The relationship isn't perfect, but as a general rule of thumb, the USD declines in years when global growth is above potential. In such years, strong global growth causes commodity prices to rise, which lifts commodity currencies. In addition, strong global growth normally triggers a flood of investment out of developed economies and into emerging economies. As emerging central banks intervene to slow the appreciation of their currencies from these two factors, they sell the USD against EUR and other alternative reserve currencies, thereby causing the USD to decline against both developed and emerging currencies. That dynamic helps explains the USD depreciation in 2017 as well as the 2004-2007 period. The 10Y average of the IMF's World GDP growth rate is 3.4% and we think that is roughly potential growth. The IMF estimates that global growth will come in at about 3.6% for 2017 and accelerate to 3.7% in 2018.

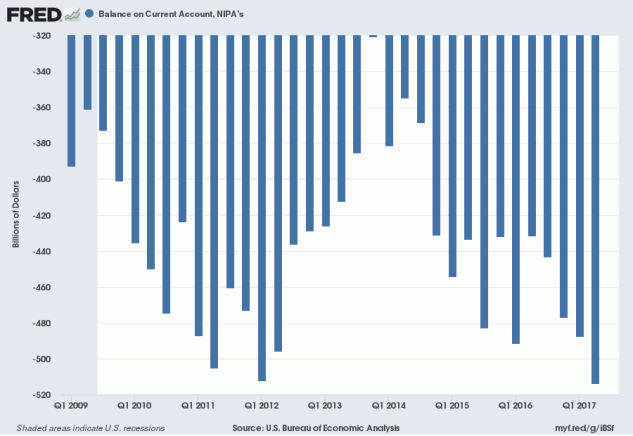

In addition, the US's twin deficit fundamental (sum of the current account deficit and fiscal or federal budget deficit as shares of GDP) is another factor that is negative for the USD. Turns in the twin deficit normally precede turns in the USD by 1-2 years and then trends match thereafter. The US's twin deficit fundamental has been deteriorating for the past two years and is likely to deteriorate further in 2018 and beyond due in part to the tax cuts. When looking at all these factors together with the fact that USD phases tend to last 5-7 years, we feel that we have to forecast a continuation of broad USD weakness—albeit at a slower pace. We project that the broad USD index will fall 1.5% in Q1 and then 1.0% per quarter in each of the remaining three quarters of 2018.

Hat tip to David Llewellyn-Smith at Macrobusiness.

The fall in the Dollar may also be self-reinforcing, as Enda Curran at Bloomberg highlights:

.....On top of the boost already coming from robust global GDP growth, the dollar's fall over the past year may add over 3 percent to the level of world trade, according to Gabriel Sterne, global head of macro research at Oxford Economics Ltd. Tipping further dollar weakness, the risks are skewed to the upside for Oxford's baseline forecast for 5 percent growth in world trade in 2018.

"Falls in the value of the dollar oil the wheels of the global financial system, boosting global liquidity by strengthening balance sheets and alleviating currency mismatches," Sterne wrote in a note. "One important channel is variation in the differential between the cost of raising dollars onshore and offshore. Dollar weakness reduces the cross-currency basis, increases cross-border lending and boosts bank equities."

The biggest winners will likely be emerging economies given the weaker dollar will lower the value of their dollar-denominated debt, taking pressure off their balance sheets and from credit conditions more generally.....

Finally, from Deutsche Bank (again hat tip to David):

How can it be that US yields are rising sharply, yet the dollar is so weak at the same time? The answer is simple: the dollar is not going down despite higher yields but because of them. Higher yields mean lower bond prices and US bonds are lower because investors don't want to buy them. This is an entirely different regime to previous years.

Dollar weakness ultimately goes back to two major problems for the greenback this year. First, US asset valuations are extremely stretched. As we argued in our 2018 FX outlook a combined measure of P/E ratios for equities and term premia for bonds is at its highest levels since the 1960s. Simply put, US bond and equity prices cannot continue going up at the same time. This correlation breakdown is structurally bearish for the dollar because it inhibits sustained inflows into US bond and equity markets.

The second dollar problem is that irrespective of asset valuations the US twin deficit (the sum of the current account and fiscal balance) is set to deteriorate dramatically in coming years. Not only does the additional fiscal stimulus recently agreed by Congress push the fair value of bonds even lower via higher issuance and inflation risk premia effects, but the current account that also needs to be financed will widen via import multiplier effects. When an economy is stimulated at full employment the only way to absorb domestic demand is higher imports. Under conservative assumptions the US twin deficit is set to deteriorate by well over 3% of GDP over the next two years.

In summary:

- Rising global growth boosts commodity prices and emerging markets

- Central banks in emerging markets then sell Dollars to slow appreciation of their local currency

- Fiscal stimulus, such as US tax cuts and infrastructure spending, lifts inflation

- Higher inflation causes a bond bear market

- Fiscal stimulus also widens the current account deficit

- Central bank selling, higher inflation, a bond bear market and wider current account deficits all cause a weaker Dollar

The risk of paying too high a price for good-quality stocks - while a real one - is not the chief hazard confronting the average buyer of securities. Observation over many years has taught us that the chief losses to investors come from the purchase of low-quality securities at times of favorable business conditions. The purchasers view the current good earnings as equivalent to "earning power" and assume that prosperity is synonymous with safety.

~ Benjamin Graham

Disclaimer

Colin Twiggs is director of The Patient Investor Pty Ltd, an Authorised Representative (no. 1256439) of MoneySherpa Pty Limited which holds Australian Financial Services Licence No. 451289.

Everything contained in this web site, related newsletters, training videos and training courses (collectively referred to as the "Material") has been written for the purpose of teaching analysis, trading and investment techniques. The Material neither purports to be, nor is it intended to be, advice to trade or to invest in any financial instrument, or class of financial instruments, or to use any particular methods of trading or investing.

Advice in the Material is provided for the general information of readers and viewers (collectively referred to as "Readers") and does not have regard to any particular person's investment objectives, financial situation or needs. Accordingly, no Reader should act on the basis of any information in the Material without properly considering its applicability to their financial circumstances. If not properly qualified to do this for themselves, Readers should seek professional advice.

Investing and trading involves risk of loss. Past results are not necessarily indicative of future results.

The decision to invest or trade is for the Reader alone. We expressly disclaim all and any liability to any person, with respect of anything, and of the consequences of anything, done or omitted to be done by any such person in reliance upon the whole or any part of the Material.

Recent Posts

Author: Colin Twiggs is a former investment banker with almost 40 years of experience in financial markets. He co-founded Incredible Charts and writes the popular Trading Diary and Patient Investor newsletters.

Using a top-down approach, Colin identifies key macro trends in the global economy before evaluating selected opportunities using a combination of fundamental and technical analysis.

Focusing on interest rates and financial market liquidity as primary drivers of the economic cycle, he warned of the 2008/2009 and 2020 bear markets well ahead of actual events.

He founded PVT Capital (AFSL No. 546090) in May 2023, which offers investment strategy and advice to wholesale clients.