Europe uneasy, but gold and crude fall

By Colin Twiggs

September 13th, 2014 1:00 p.m. AEST (11:00 p:m EDT)

Advice herein is provided for the general information of readers and does not have regard to any particular person's investment objectives, financial situation or needs. Accordingly, no reader should act on the basis of any information contained herein without first having consulted a suitably qualified financial advisor.

Weekly highlights:

- The Dollar is strengthening

- Treasury yields (long-term) are rising

- Gold and crude oil are falling

- European stocks are bearish

- US stocks remain bullish

The tenuous ceasefire in Eastern Ukraine appears to be holding, but Europe faces another challenge this week, with a Scottish referendum on independence. Predictions of financial mayhem in the event of a "Yes" vote are, I feel, exaggerated in an attempt to influence the outcome. The official position of the UK government is:

"If a majority of those who vote want Scotland to be independent then Scotland would become an independent country after a process of negotiations."

The "process of negotiations" is likely to be comprehensive and would resolve most outstanding uncertainties in an orderly fashion. There has been much debate over economic issues, but it is no coincidence that the referendum is being held in the same year as the 700th anniversary of the Battle of Bannockburn, when Scots under Robert the Bruce defeated an English army led by Edward II to regain their independence.

Stock markets

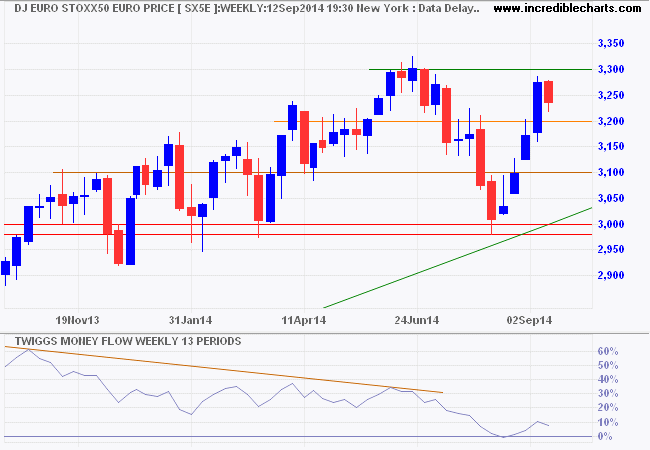

Dow Jones Euro Stoxx 50 remains hesitant, retreating from resistance at 3300. Consolidation above 3200 would be a bullish sign, while breach of 3100 would threaten primary support at 3000. Another 13-week Twiggs Money Flow trough above zero would indicate buying pressure, but reversal below zero would warn of a down-trend.

* Target calculation: 3300 + ( 3300 - 3000 ) = 3600

The S&P 500 is edging lower and follow-through below 1980 would indicate another correction. Respect of support at 1950, however, would suggest that the up-trend is intact. Sideways movement on 21-day Twiggs Money Flow, reflects further consolidation.

* Target calculation: 2000 + ( 2000 - 1900 ) = 2100

CBOE Volatility Index (VIX) below 20 is typical of a bull market.

China's Shanghai Composite Index breakout above 2250 signals a primary up-trend. The monthly chart, however, reflects further resistance at 2450/2500*. Rising 13-week Twiggs Money Flow indicates accelerating buying pressure. Reversal below 2250 is most unlikely, but would suggest further consolidation between 2000 and 2250.

* Target calculation: 2250 + ( 2250 - 2000 ) = 2500

The ASX 200 broke support at 5540/5560, warning of a correction. Bearish divergence on 21-day Twiggs Money Flow indicates medium-term selling pressure. Respect of support at 5440/5460 would indicate that the primary up-trend is intact, while a fall below 5360 would warn of a down-trend.

* Target calculation: 5650 + ( 5650 - 5450 ) = 5850

Gold & crude fall

Gold broke support at $1240/ounce to signal a primary down-trend. Declining 13-week Twiggs Momentum, below zero, strengthens the signal. Follow-through below $1200 would confirm. The sell-off is being driven by a rising Dollar.

Crude oil is also falling, with Brent Crude testing its 18-month low. Nymex breach of $92/barrel would also signal a primary down-trend.

From Nick Cunningham at Oilprice.com:

The glut of supplies and weak demand is causing problems for OPEC, according to the cartel's monthly report. OPEC lowered its demand projection for 2015 by 200,000 and in August, Saudi Arabia cut production by 400,000 bpd in an effort to stem oversupply.

It is probably no coincidence, but lower oil prices will hurt the Russian economy. As Nick points out:

Russia needs between $110 and $117 per barrel to finance its spending, which means the Kremlin can't be happy as it watches Brent prices continue to drop. Combined with an already weak economy, Russia could see its $19 billion surplus become a deficit by the end of the year.

Falling oil prices will benefit the global economy in the medium-term. Subduing Russia's territorial ambitions will be an added bonus.

That's all from me for today. Take care.

But pleasures are like poppies spread,

You seize the flow'r, its bloom is shed;

Or like the snow falls in the river,

A moment white—then melts for ever;~ Robert Burns, Tam o' Shanter (1790)

Disclaimer

Research & Investment Pty Ltd is a Corporate Authorized Representative (AR Number 384 397) of Andika Pty Ltd which holds an Australian Financial Services Licence (AFSL 297069).

The information on this web site and in the newsletters is general in nature and does not consider your personal circumstances. Please contact your professional financial adviser for advice tailored to your needs.

Research & Investment Pty Ltd ("R&I") has made every effort to ensure the reliability of the views and recommendations expressed in the reports published on its websites and newsletters. Our research is based upon information known to us or which was obtained from sources which we believe to be reliable and accurate.

No guarantee as to the capital value of investments, nor future returns are made by R&I. Neither R&I nor its employees make any representation, warranty or guarantee that the information provided is complete, accurate, current or reliable.

You are under no obligation to use these services and should always compare financial services/products to find one which best meets your personal objectives, financial situation or needs.

To the extent permitted by law, R&I and its employees, agents and authorised representatives exclude all liability for any loss or damage (including indirect, special or consequential loss or damage) arising from the use of, or reliance on, any information. If the law prohibits the exclusion of such liability, such liability shall be limited, to the extent permitted by law, to the resupply of the said information or the cost of the said resupply.

Important Warning About Simulated Results

Research & Investment (R&I) specialise in developing, testing and researching investment strategies and systems. Within the R&I web site and newsletters, you will find information about investment strategies and their performance. It is important that you understand that results from R&I research are simulated and not actual results.

No representation is made that any investor will or is likely to achieve profits or losses similar to those shown.

Simulated performance results are generally prepared with the benefit of hindsight and do not involve financial risk. No modeling can completely account for the impact of financial risk in actual investment. Account size, brokerage and slippage may also diverge from simulated results. Numerous other factors related to the markets in general or to the implementation of any specific investment system cannot be fully accounted for in the preparation of simulated performance results and may adversely affect actual investment results.

To the extent permitted by law, R&I and its employees, agents and authorised representatives exclude all liability for any loss or damage (including indirect, special or consequential loss or damage) arising from the use of, or reliance on, any information offered by R&I whether or not caused by any negligent act or omission.

Author: Colin Twiggs is a former investment banker with almost 40 years of experience in financial markets. He co-founded Incredible Charts and writes the popular Trading Diary and Patient Investor newsletters.

Using a top-down approach, Colin identifies key macro trends in the global economy before evaluating selected opportunities using a combination of fundamental and technical analysis.

Focusing on interest rates and financial market liquidity as primary drivers of the economic cycle, he warned of the 2008/2009 and 2020 bear markets well ahead of actual events.

He founded PVT Capital (AFSL No. 546090) in May 2023, which offers investment strategy and advice to wholesale clients.