China's newest export

By Colin Twiggs

January 11, 2019 8:00 p.m. ET (12:00 noon AEDT)

First, please read the Disclaimer.

"Polish authorities have arrested a Chinese employee of Huawei, the Chinese telecommunications giant, and a Polish citizen, and charged them with spying for Beijing, officials said on Friday, amid a push by the United States and its allies to restrict the use of Chinese technology based on espionage fears....

It is not the first time in recent months a Huawei employee has been arrested abroad. Meng Wanzhou, the company's chief financial officer, was arrested in Canada last month at the request of the United States, where she had been charged with fraud designed to violate American sanctions on Iran....

A 2012 report from United States lawmakers said that Huawei and another company, ZTE, were effectively arms of the Chinese government whose equipment was used for spying. Security firms have reported finding software installed on Chinese-made phones that sends users' personal data to China."

From Joanna Berendt at The New York Times

Lack of independence of private companies in China, their use for espionage purposes including industrial espionage, and failure to open Chinese markets up to foreign competitors are likely to throttle attempts to resolve trade disputes with the US. An impasse seems unavoidable.

It is important that the West confronts China over their trade tactics, espionage and 'influence' operations. Whether Donald Trump is the right person to lead this, I will leave for you to judge.

I doubt that China wants to rule the world. Dominate, perhaps. But the overriding goal of their leaders is to ensure the survival of the Chinese Communist Party (CCP). They want to make the world safe for autocracy. They don't seem to understand that this is an oxymoron. Autocracies make the world unsafe because they lack the checks and balances, imperfect as they may be, that ensure stable government in democracies whose citizens are protected by rule of law. If you think the world is already unsafe, imagine Donald Trump as president without the constraints of the US Constitution. History provides plenty of evidence of autocrats — Stalin, Hitler and Mao are prime examples — who abused their power with catastrophic results.

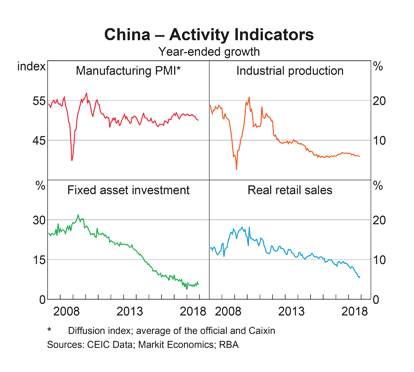

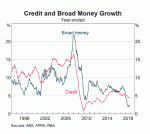

China's newest export may be a global recession if world leaders are not careful. These two charts from the RBA highlight the current state of play.

Declining growth in retail sales is accelerating. Manufacturing PMI is rolling over and industrial production is likely to follow.

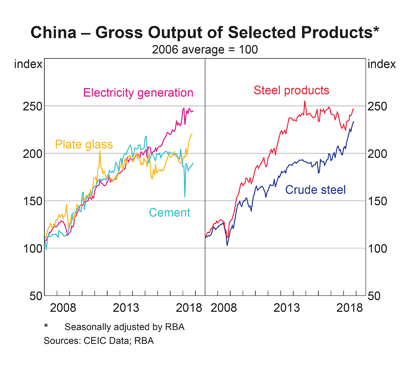

Output, on the other hand is surging, as the state attempts to spend its way out of a recession. Cement production is the sole laggard.

Matt O'Brien at The Age describes China's dilemma:

...in the depths of the Great Recession, Beijing unleashed a stimulus the likes of which the world hadn't seen since World War II.

It amounted to some 19 per cent of its gross domestic product, according to Columbia University historian Adam Tooze. By point of comparison, US President Barack Obama's stimulus was only about 5 or 6 per cent of US GDP.

Aside from its size, what made China's stimulus unique was the way it was administered. The central government didn't borrow a lot of money itself to use on infrastructure, but it pushed local governments and state-owned companies to do so.

The result was a web of debt that's been even harder to clean up than it might have been because of all the money that unregulated lenders - "shadow banks" - were frantically handing out above and beyond what Beijing had been hoping for....

What is new, though, is that this isn't working quite as well as before. As the International Monetary Fund reports, China seems to have reached a point of diminishing returns with this kind of credit stimulus.

So much new debt is either going toward paying off old debt or toward economically questionable projects that it takes a lot more of it than it used to just to achieve the same amount of growth.

Three times as much, in fact. Whereas it had only taken 6.5 trillion yuan of new credit to make China's economy grow by 5 trillion yuan per year in 2008, it took 20 trillion yuan of new credit by 2016.

I don't share Matt's conclusion that Wall Street fears the broad market will follow Apple (AAPL) into a tailspin as Chinese retail sales decline. I covered this in my last newsletter.

Nor do I think that falling Chinese steel production will plunge the global economy into recession. Though it would certainly affect Australia.

China has $3 trillion of foreign reserves and has shown in the past that it is prepared to spend big to buy its way out of a recession. Whether they succeed this time is uncertain, but old-fashioned stimulus spending will soften the impact.

I believe Wall Street has no idea how the trade dispute will play out. And financial markets have gone risk-off because of the uncertainty, despite a booming US economy.

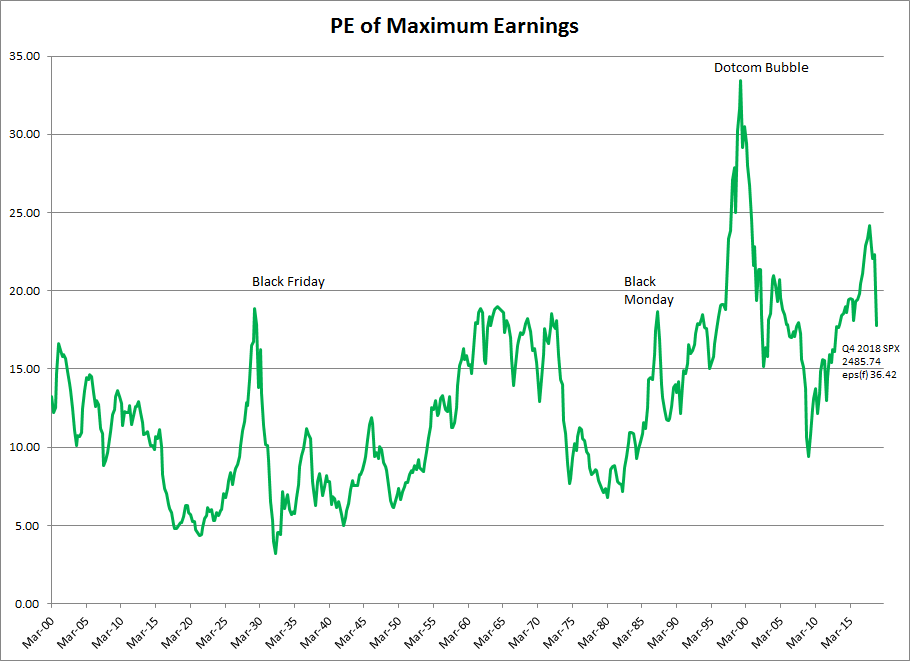

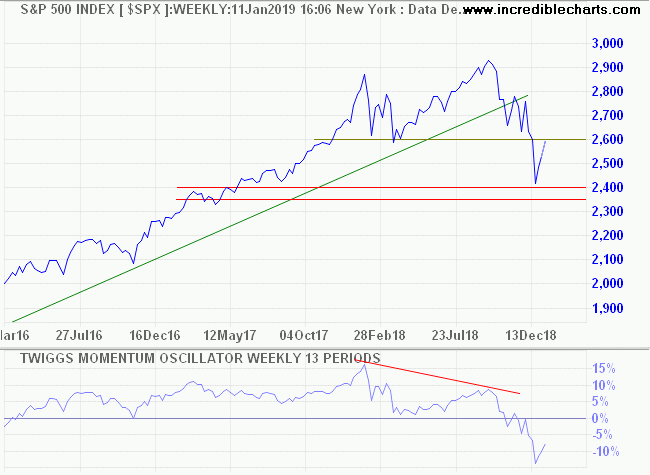

Earnings ratios have fallen dramatically, back to 17.8, from what was clearly bubble territory above 20 times historic earnings. I use the highest preceding four quarters earnings, to smooth out earnings volatility, so my P/E charts (PEmax) will look a little different to anyone else's.

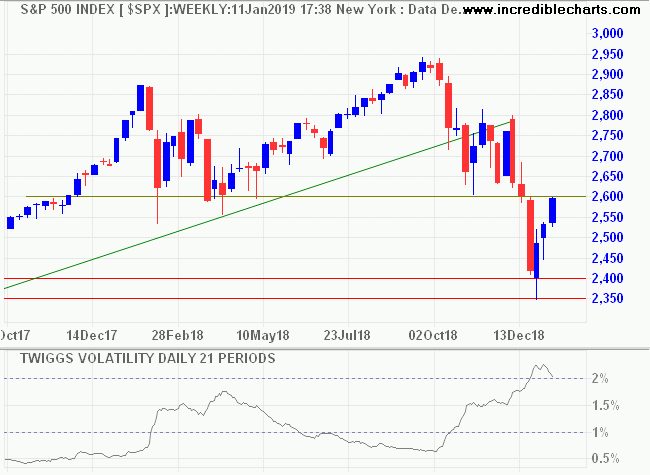

Market volatility remains high, with S&P 500 Volatility (21-day) above 2.0%. A trough above 1% on the next multi-week rally would confirm a bear market — as would an index retracement that respects 2600.

Momentum shows a strong bearish divergence.

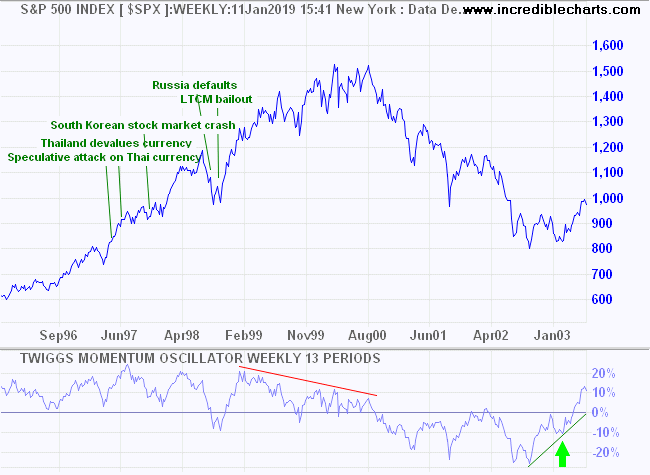

Similar to the Dotcom era below. It would be prudent to wait for a bullish divergence, as in 2003, to signal the start of the next bull market.

I repeat the same quote as last week as an important reminder, with current market volatility.

What beat me was not having brains enough to stick to my own game � that is, to play the market only when I was satisfied that precedents favored my play. There is the plain fool, who does the wrong thing at all times everywhere, but there is also the Wall Street fool, who thinks he must trade all the time.

~ Jesse Livermore

Latest

-

ASX 200

Bear market rally. -

S&P 500

S&P 500

It's a funny kind of bear market. -

Making Rational Decisions

If it's flooded, forget it. -

Portfolio

Investing in a volatile market - April 2018 -

Yield Curve

Does the yield curve warn of a recession? - September 2018

Disclaimer

Colin Twiggs is director of The Patient Investor Pty Ltd, an Authorised Representative (no. 1256439) of MoneySherpa Pty Limited which holds Australian Financial Services Licence No. 451289.

Everything contained in this web site, related newsletters, training videos and training courses (collectively referred to as the "Material") has been written for the purpose of teaching analysis, trading and investment techniques. The Material neither purports to be, nor is it intended to be, advice to trade or to invest in any financial instrument, or class of financial instruments, or to use any particular methods of trading or investing.

Advice in the Material is provided for the general information of readers and viewers (collectively referred to as "Readers") and does not have regard to any particular person's investment objectives, financial situation or needs. Accordingly, no Reader should act on the basis of any information in the Material without properly considering its applicability to their financial circumstances. If not properly qualified to do this for themselves, Readers should seek professional advice.

Investing and trading involves risk of loss. Past results are not necessarily indicative of future results.

The decision to invest or trade is for the Reader alone. We expressly disclaim all and any liability to any person, with respect of anything, and of the consequences of anything, done or omitted to be done by any such person in reliance upon the whole or any part of the Material.

Please read the Financial Services Guide.

Author: Colin Twiggs is a former investment banker with almost 40 years of experience in financial markets. He co-founded Incredible Charts and writes the popular Trading Diary and Patient Investor newsletters.

Using a top-down approach, Colin identifies key macro trends in the global economy before evaluating selected opportunities using a combination of fundamental and technical analysis.

Focusing on interest rates and financial market liquidity as primary drivers of the economic cycle, he warned of the 2008/2009 and 2020 bear markets well ahead of actual events.

He founded PVT Capital (AFSL No. 546090) in May 2023, which offers investment strategy and advice to wholesale clients.